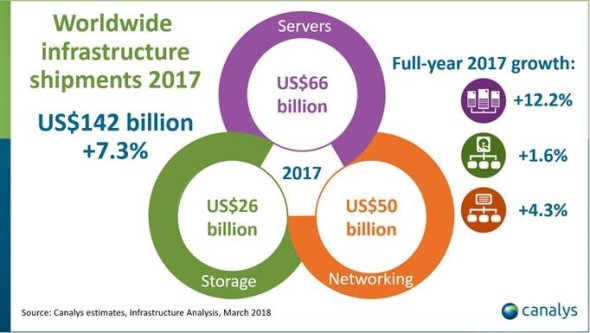

Strong growth in servers was the primary factor. Rising DRAM component costs and increasing demand for higher server specifications resulted in ASPs increasing faster than unit shipments. This, combined with ongoing data center expansion by hyperscale cloud service providers, and the start of a new enterprise refresh cycle following the launch of the next generation of Intel and AMD processors, increased server shipment value to US$66 billion. Storage returned to growth after a period of disruption, as spending moved to all-flash and software-defined products. These offset the decline in traditional HDD storage arrays. Networking continued to grow, as investment in data center switching and 11ac Wave 2 wireless LANs for campus and branch environments remained strong. Overall, Ethernet switching grew 7% and wireless LANs were up 9%. Service provider routing remained positive at 1%, but enterprise routing fell 9%.

2017 was also a strong year for the channel selling servers, storage and networking. “The channel continued to dominate infrastructure shipments, collectively representing 74% of the worldwide total,” said Canalys Principal Analyst Matthew Ball. “But direct grew faster, due to the increasing role of Chinese and Taiwanese ODM server vendors selling large volumes to cloud service providers. Direct accounted for 34% of server shipments, compared with 19% for storage and 20% for networking. The massive capital expenditure planned by the hyperscale cloud service providers in upgrading and expanding existing data centers, as well as increasing their geographic presence, will maintain this trend in 2018.”

The top three infrastructure vendors in 2017 were Cisco, Dell EMC and Hewlett Packard Enterprise (HPE), which collectively accounted for 50% of total worldwide shipments. “Cisco’s dominance in networking helped it maintain its lead of 20% in the overall infrastructure market. Its focus is on moving its predominantly hardware-centric customer base to software and subscriptions,” said Ball. “Dell EMC completed its first full year of operations, following the US$67 billion merger in September 2016, making it a leader in servers and storage. It grew its share of infrastructure shipments to 15% and was one of the fastest-growing vendors through the channel. HPE’s share of infrastructure shipments was 14%. The focus of its server business has shifted to higher-value segments, with growth in HCI and HPC. The acquisition of Nimble boosted its storage business last year, while Aruba is driving growth in wireless LANs as part of its intelligent edge strategy.”